Every so often, a property hits the market that feels like it won’t stay available for long, and hesitation can mean missing out entirely. Buyers rush to submit competitive offers, while sellers sort through multiple bids in just a few days. In that kind of fast-moving environment, traditional loan approval can feel too slow to keep up, pushing some buyers to explore alternative financing options. That’s when the question often comes up: What is a hard money loan?

Start Making Offers Without Waiting to Sell Your Home

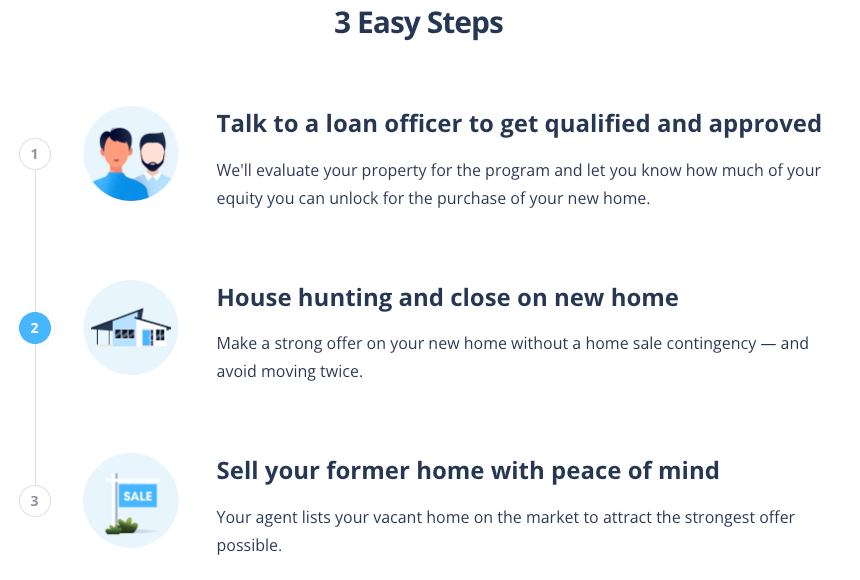

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

This type of loan is typically used by investors who want to move quickly on a fix-and-flip, as well as buyers testing the waters of rental property investing. Others turn to it when they find their next home before their current one has sold. When timing is tight and flexibility matters more than long-term rates, this type of financing can seem like a workable solution.

Here’s what you need to know about how it works, when it makes sense, what to watch out for, and which alternatives are worth exploring.

What is a hard money loan?

A hard money loan is a type of short-term financing used in real estate transactions where speed and flexibility matter more than the cost. The word “hard” in “hard money” refers to the fact that the loan is backed by a real, tangible asset, usually the property itself, as collateral.

Instead of focusing mainly on your credit score or income, lenders care more about the property’s value and profit potential. That’s why hard money loans are often used by house flippers who want to buy, renovate, and resell quickly. They’re also common for investors picking up rental properties when they need to move fast.

As with any secured loan, if a borrower defaults on a hard money loan, the lender can take ownership of the asset, such as a house, to make up for any losses.

How does a hard money loan work?

Compared to traditional financing, hard money loans move faster and are much more focused on the value of the property itself. The approval process puts more weight on the asset than the borrower’s financial profile. Here’s a quick overview of how hard money loans work, from how they’re approved to how they’re repaid.

- Short-term loan: These loans have a shorter repayment period of six to 24 months, compared to a traditional 15- or 30-year fixed mortgage loan. Some lenders will allow a 12-month extension to give borrowers a combined three-year term.

- Faster funding option: When a property purchase needs to happen quickly, a hard money loan can be approved in a few days rather than the 30 to 50 days it typically takes to complete a mortgage loan.

- Less focus on creditworthiness: Approval is not as heavily dependent on the borrower’s income or credit scores and history.

- More focus on property value: This type of loan requires collateral, such as a home, to secure the loan and is focused on the ratio of the loan amount to the value of the property.

- Non-traditional lenders: Hard money bridge loans usually come from individual investors or private lenders, not traditional banks.

- Loan denial option: A hard money loan is often used by borrowers with poor credit who have been denied a mortgage application but have significant equity in their property.

- Higher interest rates: Because the lender is exposed to more risk, hard money loans are typically more expensive than traditional mortgage loans. (See cost section below.)

- Larger down payments: In some cases, borrowers may need a larger down payment, which may be as high as 20%- 30%, depending on the property’s value and the loan circumstances.

- More flexibility: Hard money loans have less government oversight and regulation, allowing lenders to set more flexible credit score and debt-to-income (DTI) ratio criteria. They can also be used as a way to avoid foreclosure.

- Potential for interest-only payments: Unlike a traditional mortgage, a hard money lender may allow you to initially make interest-only payments or arrange for deferred payments.

Hard money loan example

Imagine you’ve found a run-down property in a promising neighborhood and plan to renovate and sell it for a profit. The purchase price is $350,000, and renovations are estimated at $50,000.

Traditional banks are hesitant due to the property’s condition, but a hard money lender sees the potential for a high resale value. They agree to lend $380,000, which covers most of the purchase price and some renovation costs, at an interest rate of 12% with a 12-month term.

This quick financing allows you to start renovations immediately and sell the property within a year for a significant profit.

When to use hard money loans

Hard money loans are used for different real estate needs, especially when someone needs fast funding or doesn’t qualify for conventional loans.

Here’s how they are typically used:

Flipping a house

For real estate investors flipping homes, hard money loans make it easier to get cash quickly to buy and renovate properties. Because they’re approved much faster than traditional loans, flippers can jump on deals in competitive markets, fix up the home, and resell it for a profit in a short amount of time.

Buying an investment rental property

Investors buying rental properties may use hard money loans to lock in a deal quickly, especially if the home needs urgent repairs before it can start earning rental income. These loans let them fix up the property and get it ready to rent much faster than going through a traditional bank.

Purchasing commercial real estate

In commercial real estate, hard money loans are often used when investors need to move quickly to close a deal before competing buyers step in. These properties may already have issues that affect their value or income potential, such as needing major renovations, being partially vacant, or requiring a shift in use to become more profitable.

That kind of situation usually needs quick access to funding, since waiting too long can mean losing the deal or letting things get worse. Traditional lenders can take weeks or even months to approve financing, which doesn’t always work in these fast-moving situations. Hard money loans help bridge that gap by giving investors faster access to cash so they can secure the property and start fixing or improving it right away.

Not being eligible for traditional loans

People who have a lot of equity in a property but don’t have great credit or have other issues that make it hard to get a traditional loan often turn to hard money loans. These loans care more about what the property is worth than the borrower’s credit history, making approval less dependent on credit scores. As a result, hard money loans for bad credit are often used by borrowers who need faster access to financing.

Facing foreclosure

Homeowners in foreclosure or near foreclosure may seek hard money loans as a last resort to refinance their debts or buy time to sell the property. This can provide a temporary solution to avoid losing their property or having a foreclosure attached to their credit report.

How much do hard money loans cost?

Hard money loans usually cost more than traditional loans because lenders are taking on more risk and offering faster, less strict funding. Here are some of the common costs you can expect with hard money loans:

- Interest rates: These can range from 8% to 15% or higher, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points, a percentage of the loan amount upfront, which can add to the initial cost of obtaining a loan.

There are many hard money loan calculators available on the Internet to give you an idea of your costs.

What are the pros and cons of hard money loans?

When traditional financing doesn’t work or moves too slowly, hard money loans can step in as a faster alternative. But while they can open doors quickly, they also come with trade-offs that borrowers need to weigh carefully. Here are the pros and cons of hard money loans.

Pros

- Fast funding: One of the biggest advantages is how quickly you can get the money. Hard money loans can often be approved and funded in just days or weeks, while traditional loans can take months.

- Flexible terms: These loans tend to be more flexible when it comes to deal structure and repayment, so lenders can sometimes adjust things based on the project and borrower’s needs.

- Easier access: If you can’t qualify for a traditional loan because of credit issues or other financial hurdles, hard money loans can offer another way to move forward with a real estate deal.

Cons

- Higher costs: The biggest downside is the price and interest. Hard money loan rates and fees are usually much higher than what you’d see with a traditional loan.

- Short repayment window: These loans often need to be paid back quickly, which can get risky if the project takes longer than expected or doesn’t go as planned.

- Property collateral risk: Since the loan is secured by the property itself, the lender can take it if you’re unable to repay, which is a major risk for borrowers.

What are some examples of hard money loan lenders?

Hard money loans are offered by a wide range of lenders, from small private investors to specialized lending companies that focus on real estate deals. Unlike traditional banks, these lenders tend to prioritize the value and potential of the property over the borrower’s credit profile. Here are some examples of hard money loan lenders you may come across.

- Flip Funding

- Groundfloor

- Kiavi

- Residential Capital Partners

- CoreVest

- Sherman Bridge

- Lima One

- RCN Capital

- Lending One

How to find and choose a hard money lender

Finding the right hard money lender can make a big difference in how smooth and successful your deal goes. Since terms, fees, and experience can vary widely, it’s important to know where to look and what to ask before committing.

Where to find lenders

- Online directories and platforms: These are websites that list and organize hard money lenders so you can easily browse your options in one place. They usually include basic info like loan types, rates, and contact details, so you can quickly compare lenders and reach out to a few that fit your needs.

- Real estate investment networks: Networking groups and referrals from other investors or agents can point you to lenders who are already trusted in real deals. These recommendations are especially helpful because they come from people with firsthand experience.

- Brokerage services: Some mortgage brokers specialize in connecting borrowers with hard money lenders. They can help match you with lenders based on your deal type, budget, and timeline.

What to ask potential lenders

- What are the interest rates, points, and all associated fees? Make sure you understand the full cost of the loan, including interest rates, upfront points, and any additional fees. These costs can add up quickly and significantly affect your overall return.

- What LTV ratios are offered, and how are they calculated (current value vs. ARV)? Ask how much of the property’s value the lender is willing to finance and whether they base it on current value or after-repair value (ARV). This will impact how much cash you need to bring to the table.

- What are the typical loan terms and repayment schedules? Get clarity on how long the loan lasts and how repayments are structured. Some loans may be interest-only with a lump-sum payoff at the end, while others may have different arrangements.

- Are there any prepayment penalties? It’s important to know if you’ll be charged for paying off the loan early. This can affect your strategy if you plan to sell or refinance quickly.

- What experience do you have with similar projects and property types? Ask whether the lender has worked on deals like yours before. Experience with similar properties can mean smoother approvals and fewer surprises.

- Are they a direct lender or a broker? Clarify whether you’re dealing directly with the money source or a middleman. This can affect pricing, speed, and how flexible the loan terms are.

What are some alternatives to hard money loans?

If a hard money loan doesn’t feel like the right fit, other financing options might work better depending on your situation. Some alternatives offer lower costs, longer repayment terms, or less risk, but they may also take more time to secure. Here are a few common alternatives to hard money loans.

- Take out a second mortgage: If you’ve built up a good amount of equity in your home, a home equity loan or a home equity line of credit (HELOC) might be a cheaper way to access cash than a hard money loan.

- Cash-out refinance: A cash-out refinance can be a more affordable way to pull equity from another property and use that money to help finance an investment purchase.

- Borrow from family or friends: A personal loan from family or friends can offer more flexible repayment terms and potentially lower or no interest rates.

- Use a government-backed loan program: Programs like those offered by the FHA, VA, or USDA can assist with buying homes, often with lower down payments and reduced interest rates.

- Consider a peer-to-peer loan: This type of loan is provided by an individual investor, a “peer” in the industry. It functions similarly to a hard money loan and can be initiated through a lending platform like Kiva, RealtyMogul, or Funding Circle.

- Explore specialized loan programs: For alternate financing, or if you already have a hard money loan and want to replace it, you might consider specialized fixer-upper or investment property refinance loans.

- Request a seller financing option: In some rare cases, sellers may agree to finance the purchase themselves, typically resulting in lower closing costs and potentially less stringent eligibility requirements.

How to buy before you sell

A hard money loan can be a helpful short-term option when you need to move fast on a new property before your current home has sold. It gives you quick access to funding so you don’t lose out on a deal while waiting for your existing sale to close.

Another option worth looking at is HomeLight’s Buy Before You Sell program. With this program, HomeLight helps you unlock the equity in your current home so you can use it toward your next purchase before your existing home officially sells. In many cases, you get an all-cash-backed offer that strengthens your position when making an offer on a new home.

Once you move into your new place, HomeLight helps coordinate the sale of your old home on the market. This setup is designed to remove the timing gap between buying and selling, so you don’t have to juggle two transactions at once.

Here’s how HomeLight Buy Before You Sell works:

»Learn more: How to ‘Buy Before You Sell’ with HomeLight

FAQs about hard money loans

Without proper planning, these loans can be risky. The higher interest rates and the short repayment periods increase the financial burden and risk. If the investment does not turn out as planned, there’s a significant risk of losing the property. With a hard money loan, it’s important to have a solid exit strategy.

Using a hard money loan to purchase a primary residence is generally not advisable due to the high interest rates and short repayment terms associated with these loans. They are primarily designed for investment opportunities with a quick return, such as flipping houses or purchasing rental properties. For a primary residence, where long-term affordability and stability are key, considering more traditional and less costly financing options might be more beneficial. You might also consider a buy before you sell program. However, if you find yourself in a unique situation where quick financing is crucial, and you have a clear, rapid repayment plan, it could be considered as a last resort.

Hard money loans are usually short-term, typically ranging from 6 months to 3 years, which can be ideal for projects expected to return profits quickly.

Yes, most hard money lenders require a down payment, which can range from 20% to 30% of the property’s purchase price, depending on the project’s risk assessment.

To find a reputable lender, start by seeking referrals from industry professionals, such as a top real estate agent in the area. Be certain to check lender credentials and histories, and review terms carefully. Always ensure they have a legitimate track record and clear, fair loan agreements. You can also check customer reviews on sites like BBB.org.

Payments are typically interest-only on a monthly basis, which means you don’t pay toward the principal loan each month. At the end of the loan term, you’ll be required to pay back the full principal amount. This can vary based on the lender and your specific agreement.

The primary requirement is sufficient equity in the property (hard asset) you are financing. Lenders will also consider your plan for the property and your financial history, though not as extensively as a traditional bank would.

While credit scores are considered, they are less critical in hard money lending than in traditional financing. Lenders focus more on the property’s value and the borrower’s equity in the property.

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Is a hard money loan right for me?

Figuring out whether a hard money loan is right for you comes down to your situation and goal. These loans usually make the most sense for deals that need to move fast or when traditional financing isn’t an option. If you’re comfortable with higher costs and shorter repayment terms in exchange for quick, flexible funding, it could be a useful tool for your next real estate investment.

That said, it’s still important to think about your long-term plan and make sure it fits your bigger financial goals. If you want help finding trusted lenders or local guidance, HomeLight can connect you with top-rated real estate agents in your area who know the market well.

If you’re a homeowner just looking to make a strong offer on a new house, consider HomeLight’s Buy Before You Sell program to unlock the equity in your current home.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

Header Image Source: (mgattorna/ Pixabay)

English (US) ·

English (US) ·