Finding the right financing in West Virginia’s real estate market can be a challenge, especially if traditional lenders aren’t an option. A hard money loan provides an alternative solution for real estate investors, house flippers, and others needing quick access to capital. Unlike conventional mortgages, these loans offer more flexibility and faster funding, which can be particularly helpful in West Virginia, where timing is everything.

Understanding hard money loans is essential if you’re considering investing in property in West Virginia or tackling a home renovation project.

We’ll break down how these loans work, who they’re suited for, and what to expect regarding costs. Plus, we’ll explore some alternatives and introduce you to a few top-rated hard money lenders in the area to help guide your decision.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

What is a hard money lender?

Hard money lenders offer short-term financing solutions to clients who need quick cash, typically for real estate investments. Their clients often include house flippers and individuals investing in rental properties who need funding to complete their projects. Instead of focusing on credit scores, hard money lenders base loan amounts on the after-repair value (ARV) of the property. ARV represents the estimated value of the property after renovations are completed.

These loans come with higher interest rates and fees than traditional mortgages because they carry more risk for the lender. Borrowers can expect rates between 8% to 15%, and fees like origination fees are usually 1% to 5% of the loan amount. If a borrower fails to repay the loan, the lender can seize the property as collateral, making it essential to understand all the terms before committing.

How does a hard money loan work?

A hard money loan in West Virginia is a unique financing option that operates differently from traditional mortgages. Here are the key features that set it apart:

- Short-term loan: These loans typically have terms ranging from 6 months to a few years, much shorter than a 30-year mortgage.

- Faster funding option: Hard money loans are known for their quick approval and funding process, often closing within 30 to 50 days.

- Less focus on creditworthiness: Hard money lenders are less concerned with your credit score, and more focused on the value of the property.

- More focus on property value: The primary consideration for hard money lenders is the property’s loan-to-value ratio and its potential for increasing in value after renovations.

- Not traditional lenders: These lenders are typically private individuals or companies, not banks or credit unions, giving them more flexibility to fund unconventional deals.

- Loan denial option: If the lender feels the property won’t provide enough security, they can deny the loan, even if the borrower meets other requirements.

- Higher interest rates: Hard money loans usually come with higher interest rates, often ranging between 8% to 15% or more, to compensate for the increased risk.

- Might require larger down payments: These loans may require down payments of 20%–30% or more, compared to a typical mortgage down payment.

- More flexibility: Hard money lenders can adjust loan terms, interest rates, and repayment schedules more easily than traditional lenders, offering greater flexibility in financing terms.

Potential for interest-only payments: Some hard money loans may allow borrowers to make interest-only payments for part or all of the loan term, with the principal due at the end.

What are hard money loans used for?

Hard money loans can be a valuable tool in several real estate situations. Below are some of the most common uses for these loans:

- Flipping a house: Investors often use hard money loans to quickly acquire properties for flipping homes. These loans help fund the purchase and renovations needed to increase the property’s value before selling it for a profit.

- Buying an investment rental property: Real estate investors may turn to hard money loans to finance the purchase of rental properties, especially if they plan to renovate the property and start generating rental income quickly.

- Purchasing commercial real estate: Investors who need to quickly secure commercial real estate deals might rely on hard money loans when time-sensitive opportunities arise, such as securing a prime business location.

- Borrowers who can’t qualify for traditional loans: Borrowers with lower credit scores or higher debt-to-income ratios may turn to hard money loans as an alternative to traditional mortgage products.

- Homeowners facing foreclosure: For homeowners at risk of losing their homes, hard money loans can provide a quick source of cash to pay off debts, prevent foreclosure, or allow them to make necessary repairs before selling.

How much do hard money loans cost?

Hard money loans generally cost more than traditional loans due to the higher risk for lenders and the convenience of quick, flexible funding. Typical costs include:

Online calculators can help estimate these costs.

Alternatives to working with hard money lenders

If a hard money loan isn’t the right fit for your financial needs, here are a few alternatives to consider:

- Take out a second mortgage: By leveraging your home equity, you can take out a second mortgage or a home equity line of credit (HELOC) at a lower interest rate than a hard money loan.

- Cash-out refinance: This option allows you to refinance an existing property, pulling out cash for other investments, often with more favorable terms than a hard money loan.

- Borrow from family or friends: Personal loans from family or friends can come with more flexible terms and lower or no interest, providing a cost-effective option.

- Use a government-backed loan program: Programs like FHA, VA, or USDA loans can help with purchasing homes or investment properties with lower down payments and interest rates.

- Peer-to-peer loan: Online lending platforms connect you with individual investors who offer loans with terms similar to hard money loans but may provide different options for repayment.

- Specialized loan programs: If you’re investing in a fixer-upper or other specific types of property, specialized loan programs could provide more suitable financing with better terms than a hard money loan.

- Request a seller financing option: In some cases, sellers may offer to finance the sale themselves, which can lower your closing costs and provide more flexibility in repayment terms.

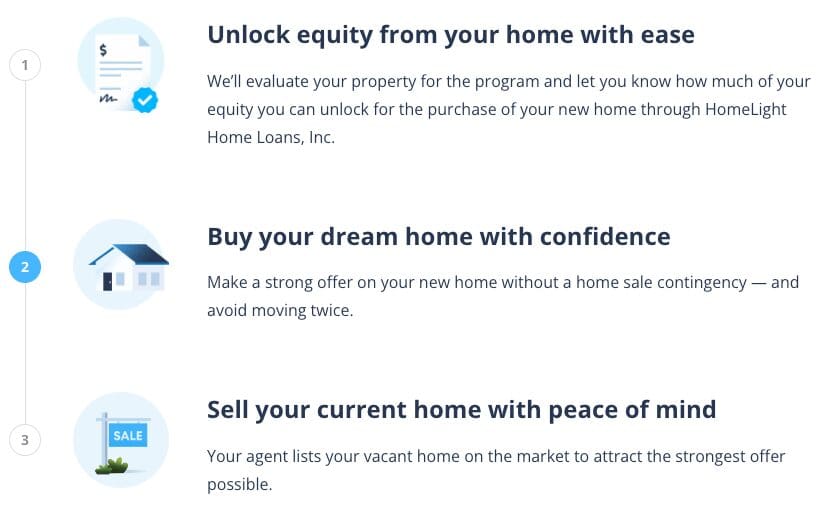

How to buy before you sell

HomeLight’s Buy Before You Sell program is designed to help homeowners purchase a new home before selling their current one. This program is especially beneficial in competitive markets like West Virginia, where timing can be critical. Instead of waiting to sell your house before making a new purchase, this program allows you to tap into your equity early, giving you the freedom to secure your dream home while still preparing your old one for sale.

The process is straightforward: HomeLight will buy your current home, allowing you to use the funds to buy a new home before selling your current one. After you’ve moved into your new property, HomeLight will list your previous home for sale.

Here’s how HomeLight Buy Before You Sell works:

Although there’s a flat fee of 2.4% of your current home’s sold price, the potential savings you could see in other areas might outweigh the cost. Once it’s sold, you’ll repay HomeLight the amount they advanced for your home purchase, plus a fee that typically ranges from 9.5% to 12%.

3 top hard money lenders in West Virginia

Traditional lenders might not be the solution for every real estate investment. If you’re looking to move quickly and capitalize on an opportunity, explore the hard money lending options available in West Virginia.

LendingOne

Founded in 2014 by Bill Green and Matthew Neisser, LendingOne addresses investor frustrations with traditional banks and hard money lenders. They offer quick approvals to foster real estate investment growth.

Lending clientele: Residential real estate investors

Loan criteria: Loan terms vary: RentalOne Portfolio offers up to 80% LTV on Purchase/Rate & Term and up to 75% on Cash Out. Portfolio Pro allows up to 75% LTV for Purchase/Refinance, and Fix to Rent provides up to 92.5% LTC.

LendingOne holds a 4.2 Google star rating from 99 reviews and has been BBB accredited since 2017.

Longhorn Investments

Founded in 2008, Longhorn Investments has funded thousands of hard money loans and operates a title company and real estate law practice from its corporate office. With expertise across residential and commercial assets, they offer short-term hard money acquisition and renovation capital in major metropolitan areas spanning Texas, Tennessee, Missouri, Indiana, Ohio, Arkansas, Alabama, New Mexico, Georgia, and North Carolina.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 70% of ARV for flips and up to 75% of ARV for rentals, excluding points and fees, with funding not exceeding 100% of the cost. Proof of refinance is required.

Longhorn Investments maintains a 5.0 Google rating from 224 reviews.

GoKapital

GoKapital is recognized as one of the leading private hard money lenders in the United States. It offers specialized mortgage solutions tailored for both seasoned and novice real estate investors.

Lending clientele: Real estate investors and entrepreneurs

Loan criteria: Up to 75% LTV and 100% of renovation costs

GoKapital has a 4.4-star rating on Google based on 40 reviews. Previous clients praise them for their professionalism and reliability.

886-257-2973

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in West Virginia?

Hard money loans can be a smart option for investors in West Virginia who need to move quickly on property deals, whether it’s for flipping houses or securing short-term financing. These loans are typically suited for those who have experience in real estate and are comfortable with higher interest rates in exchange for faster funding and more flexible terms. If timing and quick access to capital are essential, partnering with a hard money lender may be the right move for you.

However, if you’re a homeowner looking to purchase a new home before selling your current one, HomeLight’s Buy Before You Sell program offers a more predictable and potentially lower-cost solution. With this program, you can avoid the rush and pressure of selling your home before securing your next property, providing peace of mind and a smoother transition between homes.

Header Image Source: (steveheap/DepositPhotos)

English (US) ·

English (US) ·