A loan-to-value (LTV) ratio is a lender’s risk meter. It’s a number assigned to a secured loan that can either open or close doors to the funds you need to purchase or refinance a home.

The LTV percentage can also push your interest rate up or down.

In this easy guide, we’ll help you get a clear understanding of loan-to-value ratio, how to calculate it, and what different LTV ratios mean for you. We’ll also share tips to lower your loan-to-value ratio.

A Top Agent Can Help You Find A House You Can Afford

We analyze millions of home sales to find buyer’s agents who will show you the right home at the right price. Our service is 100% free, with no catch. Agents don’t pay us to be listed, so you get the best match.

What is a loan-to-value ratio in real estate?

The loan-to-value ratio (LTV) is a metric used by lenders to assess the risk of lending to you. In real estate, the LTV compares your requested loan amount to the value of the home you’d like to purchase. It’s calculated by dividing the loan amount by the appraised value of the property.

If a lender gives you a loan worth 75% of the value of the house, the LTV is 75%. Lenders consider higher LTVs to be riskier because if the loan defaults, their loss would be greater.

To mitigate this higher risk, lenders will typically charge a higher interest rate on a high LTV loan. Being on the other side of the metric works in your favor. A lower LTV usually leads to a lower interest rate.

If the LTV is over 80%, most lenders will require you to carry private mortgage insurance (PMI) which increases your monthly loan payments.

How to calculate your loan-to-value ratio

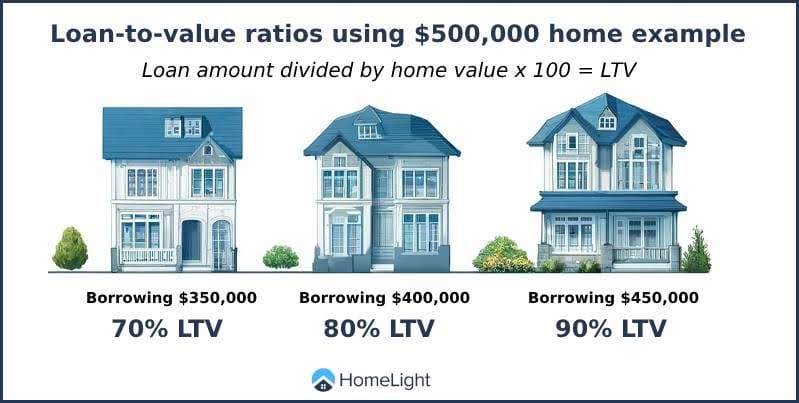

Calculating your LTV ratio is straightforward. Simply divide your mortgage loan amount by the appraised value of your home and multiply by 100 to get a percentage.

Loan amount divided by home value x 100 = LTV

If you’re buying a home appraised at $500,000 and your loan amount is $400,000, your LTV ratio is 80%

$400,000 divided by $500,000 x 100 = 80%

What is a good LTV ratio?

A good LTV ratio is typically 80% or lower. This ratio is favorable because it indicates that you will have a solid amount of equity in your home, which reduces the lender’s risk. An 80% LTV ratio often qualifies you for better interest rates and loan terms.

LVT ratio requirements by loan type

Here’s a breakdown of the LTV requirements for common types of home loans:

Conventional loan: Maximum LTV is 97%

Conventional loans typically require a maximum LTV of 97%, meaning you can finance up to 97% of the home’s value with a 3% down payment. However, to avoid private mortgage insurance (PMI), you’ll need an LTV of 80% or lower.

FHA loan: Maximum LTV is 96.5%

FHA loans, backed by the Federal Housing Administration, allow a maximum LTV of 96.5%. This means you can buy a home with as little as 3.5% down. FHA loans are popular among first-time homebuyers due to their lower down payment requirements.

VA loan: Maximum LTV is 100%

VA loans, available to veterans and active-duty service members, offer a maximum LTV of 100%. This means eligible borrowers can purchase a home with no down payment, as long as they meet the other loan requirements.

USDA loan: Maximum LTV is 100%

USDA loans, designed for rural and suburban homebuyers, also offer a maximum LTV of 100%. This allows for 100% financing with no down payment required, making homeownership accessible in designated rural areas.

Refinance: Maximum LTV varies

The maximum LTV for refinancing depends on the type of refinance. For a conventional rate-and-term refinance, the LTV can go up to 97%. For an FHA refinance, the maximum LTV is typically 97.75%. Cash-out refinances usually have lower LTV limits, such as 80% for conventional loans.

Tips to lower your LTV ratio

Lowering your loan-to-value ratio can improve your chances of loan approval and better loan terms. Here are some effective tips:

- Select a more affordable property: Opt for a home within your budget to keep the loan amount lower relative to the property value.

- Put down a larger down payment: Increasing your down payment reduces the loan amount needed, thereby lowering your LTV ratio.

- Make additional loan payments: Paying extra on your mortgage principal helps reduce the loan balance faster, improving your LTV ratio.

- Wait and let your home grow in value: Over time, property values generally increase, which can naturally lower your LTV ratio without additional payments.

- Refinance with a shorter loan term: Refinancing to a shorter-term loan can help you build equity faster, lowering your LTV ratio.

- Make home improvements: Enhancing your home’s value through improvements can increase its appraised value, thereby reducing your LTV ratio.

- Pay off other debts: Reducing your overall debt can improve your financial profile and make it easier to qualify for better loan terms.

Discover How Much Home You Can Afford With Our Home Affordability Calculator

Understand the costs associated with buying a home and find out what safe budgeting looks like.

What else impacts home loan approval?

While the loan-to-value ratio is a key metric for lenders, several other factors also influence home loan approval:

- Credit score: Lenders use your credit score to assess your creditworthiness. A higher credit score can improve your chances of approval and help you secure better interest rates.

- Debt-to-income ratio (DTI): Your DTI ratio compares your monthly debt payments to your monthly income. A lower DTI ratio indicates better financial stability and makes you a more attractive borrower.

- Employment history: Stable and consistent employment history reassures lenders of your ability to repay the loan. Lenders typically prefer borrowers with steady jobs and regular income.

- Income level: Your income level directly affects your ability to afford mortgage payments. Higher income can improve your chances of loan approval.

- Savings and assets: Having significant savings and assets can enhance your financial profile and provide a buffer for lenders, increasing your approval chances.

- Property type and condition: The type and condition of the property being financed can impact loan approval. Lenders prefer properties in good condition and in desirable locations.

LTV vs. Combined LTV: While the LTV ratio is calculated by dividing the amount of a single loan by the appraised value of the property, the combined LTV (CLTV) ratio takes into account the total amount borrowed across multiple loans against the value of the home. For example, if you have a primary mortgage and a home equity loan, the CLTV ratio would consider both loan amounts relative to the property’s value.

Find a home that fits you and your budget

A skilled agent can help you find a home that fits both your needs and your budget, ensuring you make informed decisions throughout the buying process.

Whether you’re buying, selling, or both, HomeLight can connect you with top-performing agents in your area. These agents have the expertise to guide you through every step, from understanding your LTV ratio to helping you secure the best loan terms.

Don’t leave your home search to chance — partner with a professional who can help you achieve your homeownership goals.

Header Image Source: (Curtis Adams/ Pexels)

English (US) ·

English (US) ·