Quick Read

- Washington’s $38 trillion debt and growing $2 trillion annual deficits risk raising mortgage and construction financing costs by increasing investor demands for higher returns, per analysis by the Cato Institute.

- Dennis Shea of the J. Ronald Terwilliger Center warns that rising federal debt creates uncertainty, likely leading to higher yields on U.S. Treasuries and elevated mortgage rates.

- Realtor.com Chief Economist Danielle Hale notes mortgage rates rose alongside 10-year Treasury yields despite Federal Reserve rate cuts, partially due to concerns about federal debt.

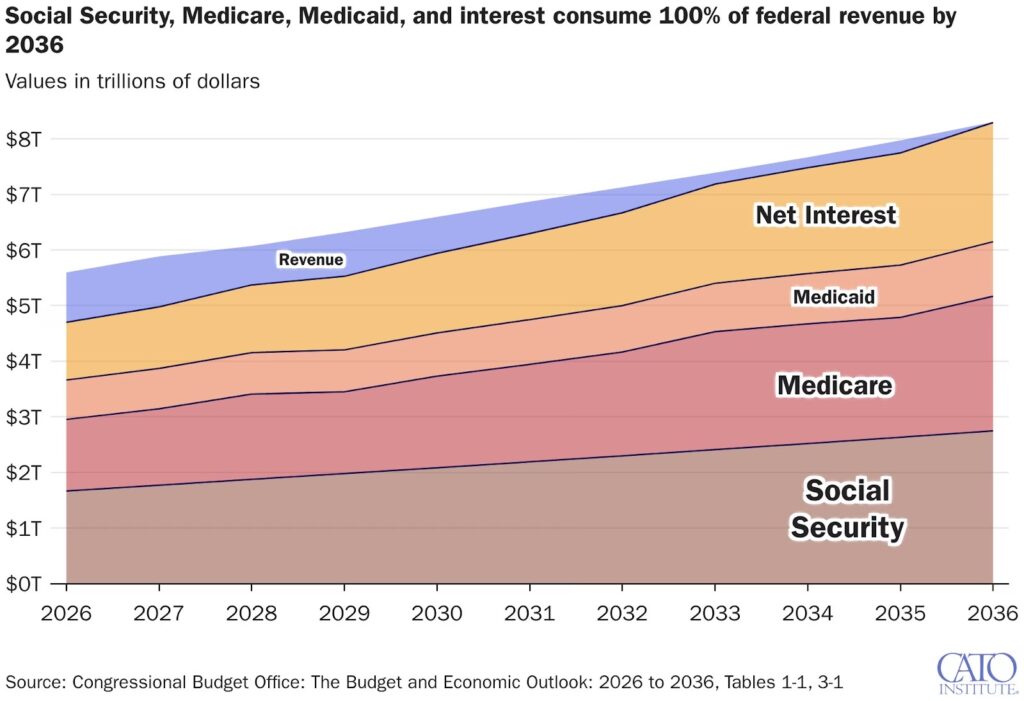

- Cato projects social programs and debt interest will consume all federal revenue by 2036, potentially crowding out private-sector homebuilder financing amid a 4.03 million-home shortage.

An AI tool created this summary, which was based on the text of the article and checked by an editor.

The next obstacle to affordable housing may not be inflation or the Federal Reserve — it could be Washington’s $38 trillion debt burden, experts say.

The next obstacle to affordable housing may not be inflation or the Federal Reserve; it could be Washington’s $38 trillion debt burden.

President Donald Trump’s fiscal 2027 budget blueprint does not lay out a clear plan to stabilize the nation’s debt, even as annual deficits grow by $2 trillion, according to an analysis by the Cato Institute. That level of debt will affect housing: Heavier government borrowing can increase financing costs if investors demand greater returns to keep lending to Washington.

“Persistent deficits and rising federal debt will create greater uncertainty about Washington’s ability to finance them,” said Dennis Shea, executive vice president and chair at the J. Ronald Terwilliger Center for Housing Policy. “The increased perception of risk will likely lead investors to demand higher yields for U.S. Treasuries, which could increase mortgage costs as well as the cost of construction financing.”

Danielle Hale | Credit: Realtor.com

The concern is not a short-term spike but the possibility that long-term rates stay elevated even as the Fed cuts short-term rates. When the Fed reduced rates by a full percentage point between September and December 2024, mortgage rates rose by roughly the same amount alongside 10-year Treasury yields, Danielle Hale, chief economist at Realtor.com, noted.

“In addition to concerns about the outlook for inflation in late 2024, some analysts suggested that rising federal debt was a driver of this disconnect,” Hale said.

Social Security, Medicare, Medicaid and interest payments on existing debt are projected to consume all federal revenue by 2036, according to Cato’s analysis. Shea also warned that rising government debt could crowd out private-sector financing available to homebuilders — adding supply-side pressure to a market already facing a 4.03 million-home shortage.

Fed Chair Jerome Powell, speaking at Harvard in March, said, “The level of the debt is not unsustainable, but the path is not sustainable.”

English (US) ·

English (US) ·